Photo by Shubham Dhage on Unsplash

Demystifying Blockchain

A Beginner's Guide to the Future of Technology

Introduction

I'm sure you've come across the term "blockchain" quite often in recent times. It's a word that's been making the rounds on the internet. If you haven't heard of it or aren't sure what it means, this article aims to provide a clear explanation.

What Is Blockchain?

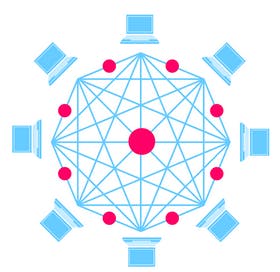

The Blockchain is like a digital ledger that keeps a record of every transaction by its users. It's like a shared document that everyone can see.

One of the main uses of blockchain is for cryptocurrencies, with Bitcoin being the most famous. Bitcoin was created by someone using the name 'Satoshi Nakamoto' in a paper called "BitCoin: A peer-to-peer electronic cash system" in 2008. A way to exchange money online without the need for a middleman. It records transactions in a decentralized digital ledger, making it immune to tampering.

How Does Blockchain Work?

Bitcoin, a digital currency, is used for online transactions involving digital assets. What makes Bitcoin special is its reliance on cryptographic proof instead of using a third party when performing transactions between two parties.

Each transaction is secured through a digital signature for added security.

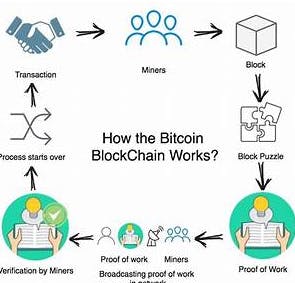

Using the knowledge above, let's explain how Blockchain works.

Starting a transaction: The process starts when a new transaction is initiated and enters the blockchain network. All the information needed is encrypted using public and private keys.

Verification: The transaction is sent to a global network of peer-to-peer computers spread across the world. Then all the nodes on the network check the validity of the transaction.

Creating a new block: After the transaction has been verified, it is added to the mempool, where together with other verified transactions it forms a block.

Consensus Algorithm: The new block is added to the blockchain network after the nodes follow a set of rules. These rules prevent the nodes from adding blocks indiscriminately.

The nodes make use of a consensus mechanism. With this mechanism, all nodes agree on which block is valid and should be added to the blockchain. The valid block is added and the node receives an incentive. After the newly created block gets its hash value and is authenticated, it is added to the open end of the blockchain.

Transaction complete: When the block is added to the blockchain, the transaction is complete and the details are stored in the blockchain for everyone to see and confirm.

The Importance of Blockchain

Blockchain has significance in today's world of tech because it can be used to securely maintain records, and also secure the exchange of assets such as money and digital items, which will create a path for technology innovation. In this section, we will cover why blockchain is important.

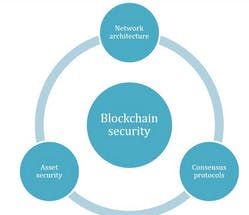

Security: The decentralized nature of Blockchain technology makes it highly secure. It is immutable thus making it resistant to data altering and fraud, This makes it important in the financial sector.

Transparency: All transactions recorded in the blockchain are transparent and verifiable. This can be used for supply chain management and voting systems.

Efficiency: Smart contracts and automation within a blockchain can simplify numerous procedures, eliminating the need for middlemen.

Data Integrity: Blockchain keeps Data safe, this feature is important for maintaining the integrity of records.

Decentralization: Blockchains remove the need for central authorities, by promoting a peer-to-peer network.

Global Access: Blockchains are globally accessible, aiding in promoting financial inclusion and promoting border-less transactions.

Immutable History: Once data is stored on a blockchain, it becomes difficult to make changes. This feature is very important for maintaining the integrity of historical records and for conducting audits.

Ownership: Blockchain allows people to have control and ownership over their digital assets, an important feature in the world of digital art and collectibles.

Brief History of Blockchain

In this section, we will provide a concise timeline overview of the history of blockchain.

In August 1991, Stuart Haber and W. Scott Stornetta introduced a cryptographic chain of blocks for timestamping digital documents, enhancing security against tampering.

Fast forward to October 2008, an individual using the pseudonym Satoshi Nakamoto released the Bitcoin whitepaper, unveiling the concept of a decentralized, peer-to-peer digital currency.

January 2009 marked the release of the Bitcoin software, along with the mining of the inaugural block known as the "genesis block," mined by Nakamoto.

By October 2011, alternative cryptocurrencies such as Litecoin emerged, expanding the blockchain ecosystem.

In November 2013, Vitalik Buterin proposed Ethereum, a new blockchain featuring a built-in programming language for smart contracts.

In July 2015, Ethereum's development received over $18 million in crowdfunding support, setting the stage for further blockchain innovation.

May 2017 witnessed the rise of Initial Coin Offerings (ICOs), which enabled blockchain projects to raise capital more easily.

May 2018 brought the introduction of the General Data Protection Regulation (GDPR) by the European Union, impacting blockchain and data privacy practices.

March 2019 saw Facebook announcing plans for the Libra cryptocurrency, later renamed Diem, leading to significant regulatory discussions.

January 2020 marked the emergence of the DeFi (Decentralized Finance) movement, offering financial services on blockchain platforms.

In February 2021, Non-Fungible Tokens (NFTs) experienced a surge in popularity, with digital art and collectibles selling for substantial amounts.

In September 2021, El Salvador made history by becoming the first country to adopt Bitcoin as legal tender.

By March 2022, central banks worldwide had begun exploring and testing Central Bank Digital Currencies (CBDCs) utilizing blockchain technology, potentially reshaping the future of digital currencies.

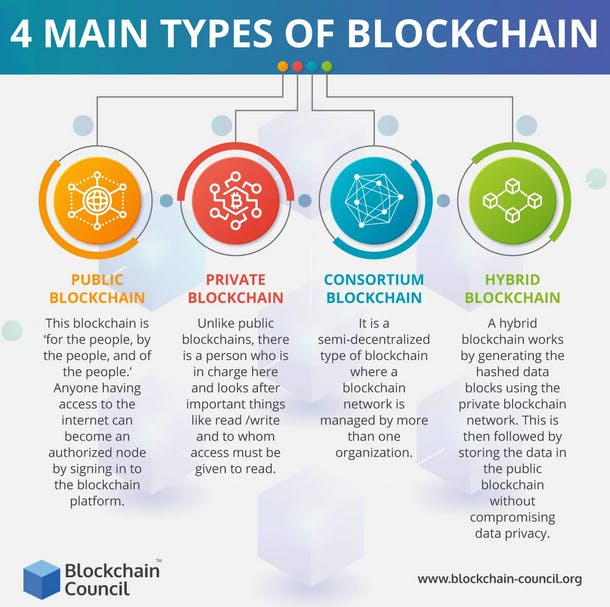

Types of Blockchains

Public vs. Private Blockchains:

Public Blockchains are open to all, decentralized, and allow anyone to participate, view, and validate transactions (e.g., Bitcoin and Ethereum). Private Blockchains are confined to specific groups or organizations, emphasizing centralization for internal use, and enhancing efficiency and security, with restricted access.

Permissioned vs. Permissionless Blockchains:

Permissioned Blockchains require known participants with prior approval, commonly used in business and enterprise for trust and privacy Permissionless Blockchains are open to all, offering greater anonymity while preserving transparency through decentralized validation

Challenges of Blockchain Technology

Scalability: Public blockchain networks, may struggle with increased transaction growth, which may lead to slower processing and increased fees as user numbers rise.

Energy Consumption: Bitcoin for example consumes substantial energy during mining, raising concerns about environmental sustainability.

Security: Despite its reputation for security, blockchain remains vulnerable to cyber threats, including attacks on individual nodes and the potential for attacks compromising its integrity.

Regulatory Uncertainty: Blockchain and cryptocurrencies face ever-evolving and uncertain regulatory landscapes, with varying international approaches, posing challenges for global adoption.

Privacy Concerns: While blockchain emphasizes transparency, it may expose sensitive information on public ledgers. Privacy-focused blockchains are emerging to address this concern.

Interoperability: Different blockchain networks may struggle to communicate and share data, limiting seamless integration into existing systems.

Lack of Standardization: The absence of universal standards in blockchain technology can hinder compatibility and widespread adoption.

Smart Contract Vulnerabilities: Smart contracts can contain coding errors or vulnerabilities that could be exploited by malicious actors, leading to financial losses.

User Accessibility: The complexity of blockchain technology can be a barrier to mainstream adoption, necessitating user-friendly interfaces and educational efforts to enhance accessibility.

Immutable Data: Once data is stored on a blockchain, making changes becomes exceedingly difficult. While this enhances security, it can be limiting in cases involving errors or disputes.

Understanding these challenges is crucial for responsible blockchain development and to unlock the full potential of this innovative technology.

Conclusion

Blockchain technology has come a long way since its inception and is now evolving into a powerful force that will have a significant impact. Its importance lies in its features of security, transparency, efficiency, data integrity, decentralization, global accessibility, and immutability.

However, blockchain is not free from challenges and limitations, which include scalability issues, energy consumption, security vulnerabilities, and regulatory uncertainties. Privacy and interoperability challenges, lack of standardization, and smart contract vulnerabilities are additional obstacles.

Addressing these challenges is an important step in ensuring that blockchain technology can fulfill its promise and continue to transform industries in the future.